In 2023, I celebrated my 10 year anniversary in the financial services industry with Ashford Advisors. I feel like 10 years of doing anything will make someone reflect a little on how far they have come and I’m certainly no different. I thought I’d put together a list of 10 core things I’ve noticed over this past decade that hopefully you find some value in or get a kick out of at the least.

- Your Savings rate is just as important, and likely more important than your rate of return.

A big question I get asked from potential clients is something along the lines of “what kind of returns have your clients received in the past x or y years?” I get the question, if I were in their shoes, I’m sure there’s a good chance I’d ask it too, but my response is usually something along the lines of this:

“Well it depends. It depends on the type of client, their risk tolerance, the purpose of the assets, etc. If I were describing a 70 year old retiree with an inherited IRA, my answer would likely be vastly different compared to a 31 year old’s Roth IRA.”

Rate of Return is of course important, but I’ve come to realize that Rate of Savings is much more critical and its also much more in our control. That’s why in one of our first meetings, we’re usually covering cash flow. Most of my clients are making any where from a couple hundred thousand dollars per year into the seven figures. When we clean up cash flow and help them with a structure that enables them to pay themselves first, some clients have been able to 3x, 4x, or 5x their saving and investing dollars monthly. For example, I’ll often meet with a new client who thinks they might be saving $1,000/month but when we clean up their cash flow, we find that really if we structure their accounts the right way and help them pay themselves first, they can go from $1,000/month to $3,000 or $4,000/month. That much of an increase in their savings rate is SO MUCH more impactful than a point here or point there difference in their returns.

**One clarification, when I say rate of savings or how much someone’s saving, I don’t mean just a savings account or money market, I’m including investments, retirement accounts, permanent life insurance, into their business, basically dollars that are earmarked for their future selves.

2. I don’t care if they went to Harvard, Yale or West Georgia. No one can predict the future. Not you, not me, nobody.

Another big question I get asked is something like “What do you think is going to happen in the stock market in the next few years, this year, etc.?”

I’ve been taught that the stock market gives many people a feeling of uncertainty because it basically moves and operates the opposite of how we live our lives. You see we live our lives with a lot of certainty day to day but if you push it out 10 years, 20 years, 30 years, the more uncertain we become. It’s the EXACT OPPOSITE in the stock market. In the stock market if you look at 1 day, you have a little better than a 50% chance you’ll be up. After a year, your odds go up to around 70%. After 10 years, you’re looking at above 90% odds you’ll be up and in 20 years, even if you had the WORST timing, there is less than a 1% chance you’d be down 20 years later.

Moral of the story, if I ask you where you’ll go out to eat on Friday night or what car you’ll be driving next week, you can tell me with pretty solid certainty but if I ask you which restaurant, you’ll frequent most in 20 years or which car you’ll be driving, your certainty plummets. The market is very uncertain short term, more certain long term.

I’ll explain the gist of this to people and even still I’ve had clients go “yeah yeah yeah, but really. What do YOU think will happen this year?”

If I knew, not sure I’d be working with many clients. As much as I love the people I work with, if I could predict the future, I’d probably be running only my own money from the beach or the country club clubhouse.

3. Personal finance has some true parallels to the fitness/nutrition industry. Mainly, it's something that is MUCH easier said than done.

Move more, eat less. Pretty simple, right? Than why do so many Americans, (myself included) struggle to work out as much as they should or eat as well as they should? Human behavior.

Vanguard, JPMorgan, Dalbar, have all put out investor studies over the years showing that the avg. market return has been around let's say 10% while the typical investor has only received roughly 3%. How could that be? Because “Buy low, sell high” is about as easy as “Eat less, Move more.”

This is totally my opinion. But after 10 years of doing this, I’m convinced that *most* people, not all, without someone like me will not do the following:

-Complete their estate planning and legal documents through the help of an attorney

-Acquire the right types and right amounts of protection and insurance coverages

-Save 15-20% of their gross income (here’s the average)

-Realize anywhere close to the 10% return they think they’re entitled to in Capital Markets

-Effectively leave money to themselves or their heirs.

-Be optimal from a tax efficiency standpoint.

4. “Things change, Mox”

As a 90’s kid, Varsity Blues is one of my favorite all time movies and when Darcy Sears dropped that line on Jonathan Moxon, of course, now I see it in personal finance.

I was at a conference in the tail end of 2020 and the keynote speaker was asked what she thought it would be like when we reach NEGATIVE interest rates in the U.S. It had happened in some international markets and interest rates here domestically we’re in the basement. 30 year mortgages were going for under 3% for some borrowers, online savings accounts were paying 0.5% and very quickly, things changed. Mortgages we’re around 8% in the fall of 2023 and you can now find savings accounts paying 4%, 5% or more.

Bottom line, be careful with your assumptions. It's very easy to say “oh well this will never happen” and then plan your future where you could fail if that one thing (inflation, interest rate swings, market corrections, to name a few) did happen. Things change but also on the flip side….

5. “The more things change, the more they stay the same”

Some things are just “Tried and True” it seems. Nothing gets my eyes rolling more than when I hear “oh XYZ is DEAD.” Or “ABC is a SCAM!”

Here are some examples:

“Value investing is dead”

“The 60/40 stock and bond portfolio is dead”

“Permanent/Cash Value Life Insurance is a scam!”

Value stocks have historically outperformed growth stocks by more than 4% since 1927. Of course, during covid, interest rates were low, money was cheap and growth stocks went on a tear. Many “gurus” declared value to be dead and gone.

A 60/40 portfolio has been a staple in the investment arena for decades, getting much of the market returns but with much less risk or standard deviation. 2022, however saw a historically tough year for bonds AND stocks so when this happened, the “gurus” called the time of death. “December 31st, 2022, time of death, 11:59, call it.” Of course this year, a 60/40 sample allocation is off to a fine start.

Dividend participating, permanent, whole life insurance has been around since the 1800’s but if you ask around, you’re bound to find someone who’s not a fan. It tends to be a little polarizing, I mean as polarizing as something as exciting or sexy as life insurance can be... There are plenty of "personalities” or brothers in law or whoever that might tell you that “just buy term life and throw the rest in an index fund.” Ernst and Young shows otherwise. https://www.ey.com/en_us/insurance/how-life-insurers-can-provide-differentiated-retirement-benefits

It’s also such a bad deal and a bad financial product, that Clemson, Penn State and Michigan are putting hefty sums of permanent life premiums in the contracts of their football coaches. I went to a real college though (Isn’t West Georgia considered Southern Ivy League?), so what would they know?

- You don’t have to be a “Do it yourselfer” or “DIY”

I see so many self proclaimed “financial gurus” on social media who claim if you buy their book or buy their course, that they will teach you personal finance from A-Z so that you can do this yourself. The question is, do you even want to? Are you a natural do it yourselfer?

You see, I am not that guy. I don’t cut my own grass, file my own taxes, navigate the real estate market alone, it's just not me. I. Value. People.

I value professionals who do this every day, who understand our situation and I want sharp people like that in my corner when the chips are down and the stakes are high.

Take a 35 year old couple. Let's say they each make $150,000 per year. If they work to age 65 and earn an average income increase of 4%, the cumulative amount of money they’re going to make is $16,830,000.

$16.8 Million Dollars. With that much at stake, are you absolutely sure you don’t want someone who does this every day, who has spent a decade or more helping clients build and protect their balance sheets by your side?

Now full disclosure, I HAVE met some folks in ten years that I think are pretty well suited to do this on their own, but it's less than a handful.

- This is a behavior sport and a lifelong one.

A couple of years ago, I was working with a nutritionist on my own physical health. We were reviewing macros, micros, blood sugar, blood pressure. You name it.

During one of our sessions she told me that she wanted her and her husband to sit down with me to discuss their financial situation. Of course, I was more than happy to help but she explained to me that she was looking for more of a short term, project based relationship, similar to the way she works with her clients.

I respectfully declined and here’s why I’m building what are hopefully lifelong or at least career long relationships with clients. You see in nutrition and fitness, she could have set me up perfectly and in complete alignment with my personal circumstances and goals but if I have a bad day or two behaviorally with my fitness and nutrition, I can recover from that. I can get right back on track and not have a permanent loss from my progress.

In finance, it is the complete opposite. One or two behavior decisions per decade and you might as well have stuffed your money in your mattress. You could have sold to cash in April of 2020, 2008, 2000, 2001, 2002, it could have a permanent impact on your balance sheet. Something bad could happen to you or a family member, without the proper protection in place, you could be looking at a permanent loss on your balance sheet. There is no “end zone” to this. Its like golf or tennis, its a sport that you (hopefully) play for life.

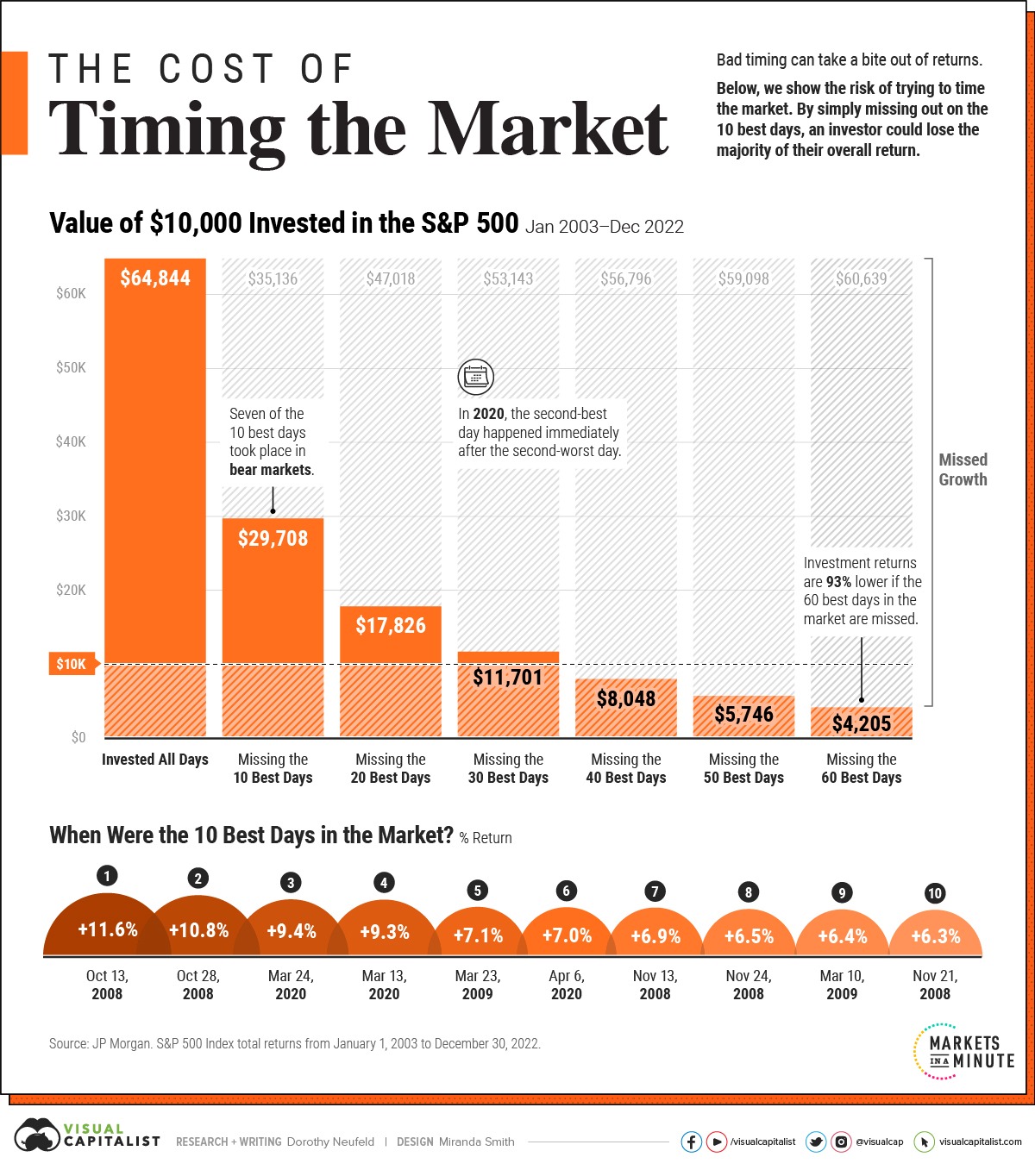

- Time In the Market, Is much more critical than Timing the market.

From 2003 to the end of 2022:

- Cash (or liquidity) is King!

Something that I benefited from but that was completely out of my control was the year I graduated from college, 2012. People were still fragile from the 2008 global financial crisis but for the most part, the economy had recovered. I began my career in the early stages of one of the biggest bull markets that we’ve ever seen. Eventually, a disturbing trend I started to see was with some folks who didn’t want to carry much cash on their balance sheet because not only were markets on fire but we were also in a historically low interest rate environment. Markets were cruising and you could barely get 1-2% in a savings account or money market account so why bother?

The same reason that Warren Buffett’s Berkshire Hathaway is sitting on a $157B cash position. Cash and liquidity are great to have for opportunities that come across your desk or unfortunately, if an emergency comes across.

How many folks do you know that have been laid off between 2022 and 2023? I bet it's more than zero. My clients who have good liquidity are sleeping better at night, have more options at their disposal and are equipped to handle life’s speed bumps. This is especially true in the current economic environment and also at the beginning stages of Covid back in the spring of 2020.

Our target is to ultimately build up 1 year’s worth of income in liquid sources and the above is the reason why. Back to the behavior issue in points 7 and 8. Sometimes a behavior decision isn’t a psychological one. It might not be fear of markets, someone might be FORCED into a behavioral error, selling low because of a life event that pops up and they don’t have the cash or cash equivalents to turn to so they’re forced to sell market based assets at a loss.

- I’ve got your back and I believe in you.

Dealing with human beings, families and the emotions that come with money can be taxing but it's something that is totally worth it and something I immensely enjoy in my career. What I’ve learned is that the vast majority of people really do love their families and they’re doing the best they can. I empathize with my clients, family and friends there. Life is hard. We’re tired, a lot of us have kids and spouses, parents, dreams and desires, fears and stress and we’re all just doing the best we can. I’m here to tell you that you and your family are worth it. We all work so hard to provide and care for the people we love, we are literally trading a huge part of our time and our life for money, and I want the money part to mean something meaningful and impactful for you. You deserve it.

https://www.dimensional.com/us-en/insights/when-its-value-versus-growth-history-is-on-values-side

https://corporate.vanguard.com/content/corporatesite/us/en/corp/articles/improved-outlook-60-40.html

https://www.globalfd.com/blog/colleges-coax-elite-coaches-with-split-dollar-life-insurance/

https://portfolioslab.com/portfolio/stocks-bonds-60-40

https://www.ey.com/en_us/insurance/how-life-insurers-can-provide-differentiated-retirement-benefits

https://eh.net/encyclopedia/life-insurance-in-the-united-states-through-world-war-i/

https://www.wsj.com/finance/stocks/warren-buffetts-berkshire-hathaway-sits-on-record-157-billion-cash-pile-3777dd4b?st=2sz02hqpujh8ci8&mod=googlenewsfeed